FIN 650 Benchmark Mini Case 4: Stock Valuation, Free Cash Flow, and Ethical Standards in Corporate Expansion

Stock valuation using the Free Cash Flow (FCF) valuation model is the central focus of FIN 650 Benchmark Mini Case 4, which challenges students to analyze the potential acquisition of Biggerstaff & McDonald (B&M), a privately held company with $24 million in free cash flow growing at 5% annually, using a Weighted Average Cost of Capital (WACC) of 11%. The assignment also requires a 250–500 word report on ethical standards in business as they apply to corporate expansion. This guide provides a comprehensive, step-by-step breakdown of every question in both Part 1 and Part 2, designed to be the single most authoritative resource for completing this benchmark assignment.

Benchmark – Mini Case 4

The purpose of this assignment is to explain core concepts related to stocks and to analyze the ethical implications of decisions and promote ethical standards within organizations.

Read the Chapter 7 Mini Case in Financial Management: Theory and Practice With MindTap. Complete Parts 1 and 2.

Part 1: Using complete sentences and academic vocabulary, please answer questions a through d.

Part 2: Using the mini case information, write a 250-500-word report presenting potential ethical issues that may arise from expanding into other related fields. In your discussion, proactively strategize about possible expansion by explaining opportunities to promote ethical standards within your organization.

While APA style is not required for the body of this assignment, solid academic writing is expected, and documentation of sources should be presented using APA formatting guidelines, which can be found in the APA Style Guide, located in the Student Success Center.

This assignment uses a rubric. Please review the rubric prior to beginning the assignment to become familiar with the expectations for successful completion.

You are required to submit this assignment to LopesWrite. A link to the LopesWrite technical support articles is located in Class Resources if you need assistance.

Mini Case

Your employer, a midsized human resources management company, is considering expansion into related fields, including the acquisition of Temp Force Company, an employment agency that supplies word processor operators and computer programmers to businesses with temporarily heavy workloads. Your employer is also considering the purchase of Biggerstaff & McDonald (B&M), a privately held company owned by two friends, each with 5 million shares of stock.

B&M currently has free cash flow of $24 million, which is expected to grow at a constant rate of 5%. B&M’s financial statements report short-term investments of $100 million, debt of $200 million, and preferred stock of $50 million. B&M’s weighted average cost of capital (WACC) is 11%. Answer the following questions:

- Describe briefly the legal rights and privileges of common stockholders.

- What is free cash flow (FCF)? What is the weighted average cost of capital? What is the free cash flow valuation model?

- Use a pie chart to illustrate the sources that comprise a hypothetical company’s total value. Using another pie chart, show the claims on a company’s value. How is equity a residual claim?

- Suppose the free cash flow at Time 1 is expected to grow at a constant rate of forever. If, what is a formula for the present value of expected free cash flows when discounted at the WACC? If the most recent free cash flow is expected to grow at a constant rate of forever (and), what is a formula for the present value of expected free cash flows when discounted at the WACC?

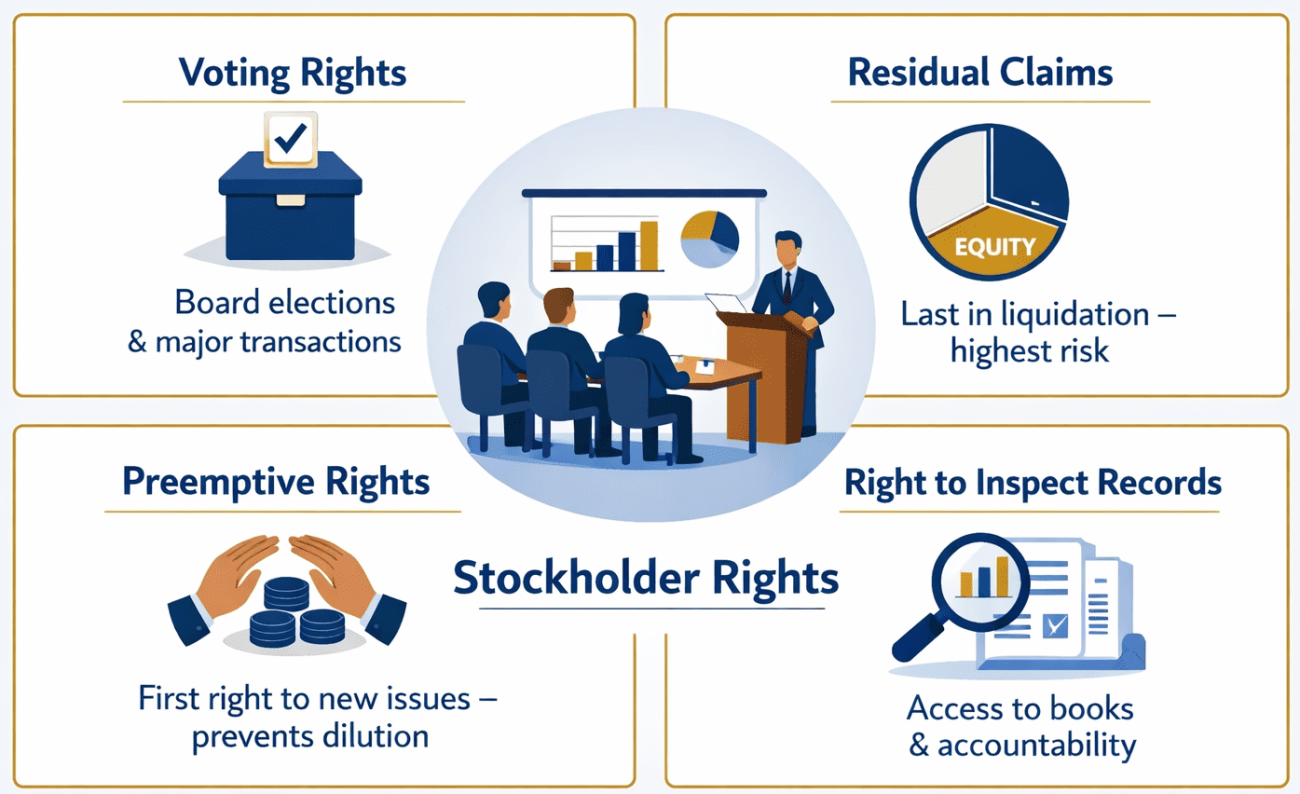

What Are the Legal Rights and Privileges of Common Stockholders?

Common stockholders hold four fundamental legal rights that govern their relationship with a corporation: voting rights, residual claims, preemptive rights, and the right to inspect financial records.

These rights are not merely procedural; they define the power structure of corporate governance. Understanding them is the foundation upon which all stock valuation models are built.

Voting Rights

Common stockholders have the right to vote on major corporate decisions, including the election of the board of directors and approval of significant transactions such as mergers, acquisitions, and major asset sales. Each share typically carries one vote, though some corporations issue dual-class stock structures with differentiated voting power.

Residual Claims on Assets and Earnings

Common stockholders are residual claimants, meaning they receive distributions only after all creditors and preferred stockholders have been paid. In a liquidation scenario, this places common equity last in the priority hierarchy; behind bondholders and preferred shareholders. This residual nature is precisely why equity is the riskiest capital component and commands the highest required rate of return.

Preemptive Rights

The preemptive right grants existing stockholders the first opportunity to purchase newly issued shares in proportion to their current ownership stake. This protection prevents equity dilution — a situation where new share issuance would reduce existing shareholders’ percentage of ownership and, consequently, their voting power and claim on earnings.

Right to Inspect Financial Records

Stockholders are entitled, within statutory limits, to examine a corporation’s financial statements and books. This transparency requirement reinforces corporate accountability and supports informed investment decision-making.

What Is Free Cash Flow (FCF) and Why Does It Matter for Valuation?

Free Cash Flow (FCF) is the cash generated by a firm after accounting for all operating expenses and capital expenditures; the actual cash available for distribution to all capital providers, including debtholders, preferred stockholders, and common stockholders.

Unlike net income, FCF is not subject to accrual accounting distortions. It reflects the true economic engine of a business, making it the preferred basis for corporate valuation among financial analysts and investment professionals.

The FCF Formula

FCF can be derived as:

FCF = Net Operating Profit After Tax (NOPAT) − Net Investment in Operating Capital

Or alternatively:

FCF = Operating Cash Flow − Capital Expenditures

In the B&M case, free cash flow is $24 million, expected to grow at a constant rate of 5% per year. This steady, predictable growth rate is what makes the constant-growth FCF valuation model directly applicable.

What Is the Weighted Average Cost of Capital (WACC)?

WACC is the blended required rate of return across all sources of capital — debt, preferred stock, and common equity — weighted by each component’s proportion in the firm’s capital structure.

The formula is:

WACC = wdrd(1 − T) + wpsrps + wcers

Where:

- wd = weight of debt

- rd = cost of debt

- T = tax rate

- wps = weight of preferred stock

- rps = cost of preferred stock

- wce = weight of common equity

- rs = required return on equity

In the B&M mini case, WACC = 11%. This rate is critical because it serves as the discount rate in the Free Cash Flow Valuation Model. If WACC increases, the estimated value of operations falls — and vice versa.

What Is the Free Cash Flow Valuation Model?

The Free Cash Flow Valuation Model estimates a firm’s value of operations as the present value of all expected future free cash flows, discounted at the WACC.

The constant-growth version of the model is:

V(ops) = FCF₁ ÷ (WACC − g)

Where:

- FCF₁ = Free cash flow at the end of Year 1

- WACC = Weighted average cost of capital

- g = Constant growth rate of FCF (must be less than WACC)

This model is analogous to the Gordon Growth Model used in dividend discount valuation, except it operates at the firm level rather than the equity level — making it especially useful for valuing privately held companies like B&M that may not pay dividends.

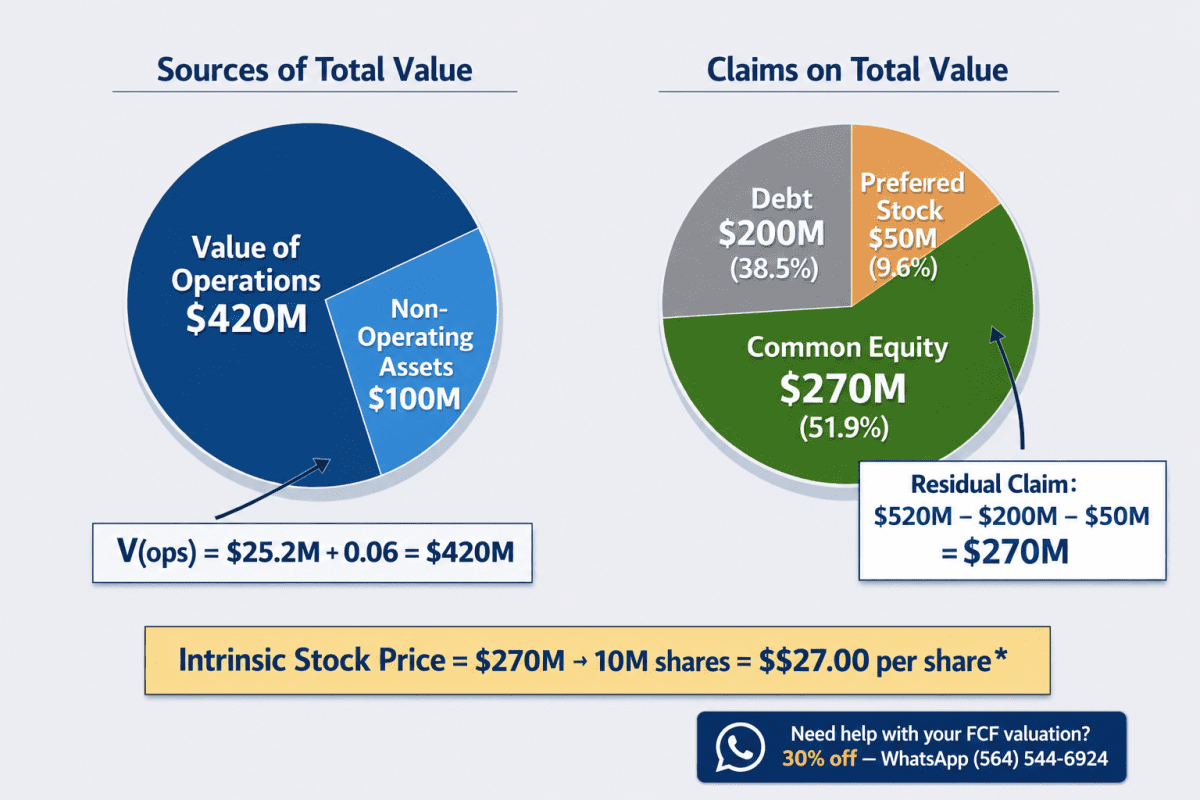

How Do You Illustrate the Sources and Claims on a Company’s Value?

A company’s total value can be divided into two categories: its value of operations and its non-operating assets, most commonly short-term investments or marketable securities.

Pie Chart 1: Sources of Total Value

For a hypothetical firm, total corporate value is the sum of:

- Value of Operations — the present value of expected future FCFs

- Non-Operating Assets — assets not directly tied to operations, such as cash equivalents or short-term investments

Applied to B&M:

- Value of Operations: $420 million

- Short-Term Investments: $100 million

- Total Corporate Value: $520 million

Pie Chart 2: Claims on Total Value

The claims side shows who has a financial interest in that $520 million:

- Debt: $200 million (38.5%)

- Preferred Stock: $50 million (9.6%)

- Common Equity (Intrinsic Value): $270 million (51.9%)

Why Is Equity a Residual Claim?

Equity is a residual claim because common stockholders receive what remains after all other financial obligations are satisfied. In the B&M scenario, once debt ($200M) and preferred stock ($50M) claims are subtracted from total corporate value ($520M), the residual, $270 million, belongs to common stockholders.

This residual nature has a direct implication for risk: equity holders bear the greatest downside risk (potentially receiving nothing in a bankruptcy scenario) but also capture all of the upside if the firm performs beyond expectations.

What Are the Present Value Formulas for Expected Free Cash Flows?

The present value of expected free cash flows depends on whether you begin with the next period’s FCF (FCF₁) or the most recent FCF (FCF₀).

Both formulas assume a constant growth rate gL that is less than WACC; a necessary mathematical condition for the model to produce a finite, positive value.

Formula 1: Starting with FCF₁

When FCF at Time 1 is expected to grow at a constant rate gL forever:

V(ops) = FCF₁ ÷ (WACC − gL)

This is used when the Year 1 free cash flow is already known or explicitly given.

Formula 2: Starting with FCF₀ (Most Recent FCF)

When the most recent free cash flow FCF₀ is expected to grow at a constant rate gL forever:

V(ops) = FCF₀(1 + gL) ÷ (WACC − gL)

This version grows FCF₀ by one period to arrive at FCF₁ before discounting. The two formulas are mathematically equivalent when FCF₁ = FCF₀(1 + gL).

Applying the Formula to B&M

Using B&M’s data:

- FCF₀ = $24 million

- gL = 5% (0.05)

- WACC = 11% (0.11)

V(ops) = $24M × (1.05) ÷ (0.11 − 0.05) V(ops) = $25.2M ÷ 0.06 V(ops) = $420 million

Total Corporate Value = $420M (operations) + $100M (short-term investments) = $520 million

Intrinsic Value of Equity = $520M − $200M (debt) − $50M (preferred stock) = $270 million

Intrinsic Stock Price Per Share = $270M ÷ 10 million shares = $27.00 per share

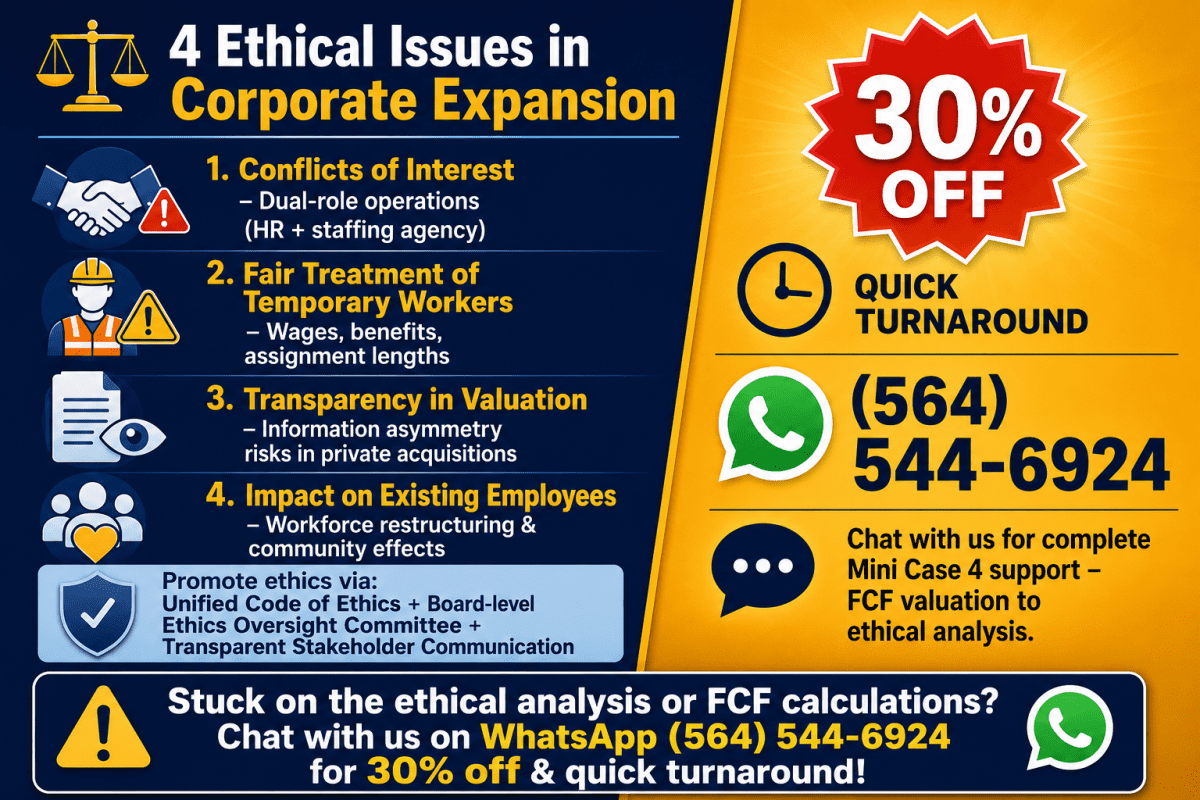

What Ethical Issues Arise From Corporate Expansion Into Related Fields?

Corporate expansion into related fields introduces a range of ethical issues; from conflicts of interest and worker exploitation to transparency obligations toward shareholders and responsibilities to newly acquired employees.

For a midsized human resources management company acquiring both a temporary staffing agency (Temp Force) and a privately held firm (B&M), these risks are not hypothetical. They are structurally embedded in the nature of the acquisitions.

Ethical Issue 1: Conflicts of Interest in Dual-Role Operations

When an HR management company acquires a staffing agency, it simultaneously serves employers and job-seekers, creating a structural conflict of interest. The firm’s fiduciary duty to its corporate clients may come into direct tension with its ethical responsibility to the temporary workers it places.

Decisions about worker wages, assignment lengths, and benefits could be influenced by the profitability goals of the parent company rather than the well-being of placed workers. Proactively establishing a clear ethical charter that separates advisory functions from staffing operations is essential.

Ethical Issue 2: Fair Treatment of Temporary Workers

Temporary workers are among the most economically vulnerable segments of the workforce, and the acquisition of Temp Force creates a direct ethical obligation to uphold fair labor standards. Research from the Economic Policy Institute has documented that temporary workers consistently earn less than their permanent counterparts in equivalent roles and receive fewer benefits.

The company must evaluate whether its post-acquisition operational model will maintain or improve those standards; not merely comply with minimum legal requirements.

Ethical Issue 3: Transparency in the Valuation and Acquisition Process

Privately held company acquisitions carry inherent information asymmetry risks, as the target firm (B&M) is not subject to the same disclosure requirements as a publicly traded company. Executives have an ethical obligation to conduct thorough due diligence and disclose all material findings to the board and shareholders.

Selective disclosure, presenting only favorable financial projections, would constitute a breach of fiduciary duty and undermine stakeholder trust.

Ethical Issue 4: Impact on Existing Employees

Corporate acquisitions frequently result in workforce restructuring, and the ethical dimension of those decisions extends beyond legal compliance. Employees at acquired firms, especially those at a privately held company like B&M, may not have the same protections as employees at publicly traded firms.

Leadership must proactively communicate integration plans, protect institutional knowledge holders, and avoid using the acquisition as a pretext for cost-cutting layoffs that damage communities.

How to Promote Ethical Standards During Corporate Expansion

Promoting ethical standards during expansion requires embedding ethics into governance structures, not merely issuing policy statements. The following strategies provide a proactive framework for the acquiring HR management company.

Strategy 1: Establish a Unified Code of Ethics

Develop and publish a comprehensive code of ethics that explicitly applies to all acquired entities from the day of integration. The code should address conflicts of interest, fair labor standards, data privacy, and financial disclosure.

Strategy 2: Create an Ethics Oversight Committee

Establish a board-level Ethics and Compliance Committee with the authority to audit practices, receive anonymous reports, and recommend corrective action. This structure signals that ethical accountability exists at the highest level of governance.

Strategy 3: Transparent Stakeholder Communication

Commit to transparent communication with all stakeholders, employees, shareholders, clients, and placed workers, throughout the acquisition and integration process. Silence during transitions breeds distrust; proactive communication builds organizational resilience.

Strategy 4: Embed Ethical KPIs in Executive Performance Reviews

Tie a percentage of executive compensation to measurable ethical outcomes: employee satisfaction scores, ethics training completion rates, whistleblower response times, and audit results. This aligns financial incentives with ethical behavior; a critical structural fix.

Strategy 5: Ethics Training as Standard Onboarding

Require all employees at acquired companies to complete ethics training within their first 30 days. The training should be scenario-based, relevant to their specific roles, and refreshed annually.

Frequently Asked Questions (People Also Ask)

What is the difference between FCF and net income in valuation?

Net income is an accounting measure subject to non-cash adjustments; FCF is a cash-based measure that reflects actual economic value generation. FCF excludes depreciation distortions and includes the capital expenditure requirements of a business, making it a more reliable basis for corporate valuation. Financial theorists, including Brigham and Ehrhardt (Financial Management: Theory and Practice), argue that FCF-based valuation models are superior for privately held firms where dividend data is unavailable.

Why must the growth rate (g) be less than WACC in the FCF model?

If g equals or exceeds WACC, the denominator in the FCF valuation formula becomes zero or negative, making the result mathematically undefined or economically meaningless. In practice, no firm can sustain growth above its cost of capital indefinitely, as that would imply the firm becomes larger than the entire economy over time. The condition gL < WACC is both a mathematical requirement and an economic reality check.

How is the intrinsic stock price per share calculated in the B&M case?

The intrinsic stock price per share is calculated by dividing the intrinsic value of equity by the total number of shares outstanding. In the B&M case: total corporate value ($520M) minus debt ($200M) minus preferred stock ($50M) equals equity value ($270M), divided by 10 million shares (5 million each owned by two friends), equals $27.00 per share.

What are common stockholders’ rights in a corporate acquisition?

In a corporate acquisition, common stockholders typically have the right to vote on the transaction and, in some cases, to receive appraisal rights; meaning they can demand a court-determined fair value for their shares if they disagree with the acquisition price. The preemptive right generally does not apply in acquisition scenarios, but shareholder approval thresholds (often two-thirds of outstanding shares) provide a meaningful governance check.

How should a company balance financial goals and ethical standards during expansion?

Financial goals and ethical standards are not inherently in conflict; companies with strong ethical cultures consistently demonstrate lower long-term risk profiles and higher stakeholder loyalty. Research published by the Ethics & Compliance Initiative (ECI) shows that organizations with strong ethics programs are three times more likely to be reported as high-performing by employees. Embedding ethics into governance structures, rather than treating it as a compliance checkbox, is the most effective strategy for sustainable value creation during expansion.